THE WEEK ON WALL STREET

Investors rode a rollercoaster of emotions as rising hostilities at the Russian-Ukrainian border sent stocks sharply lower before a powerful late-week rally erased early losses.

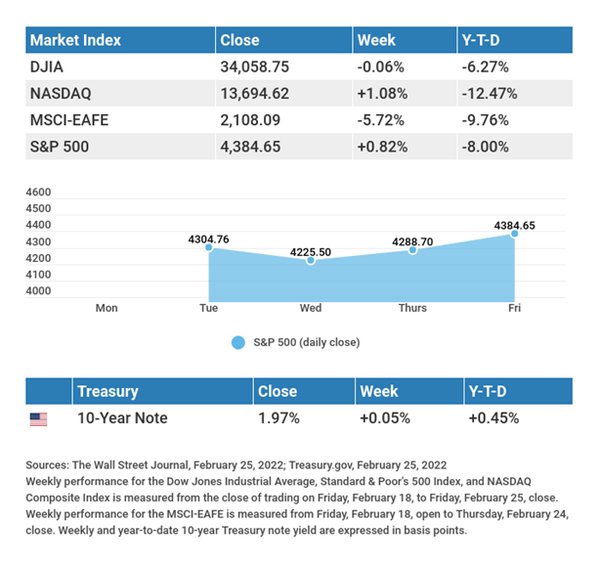

The Dow Jones Industrial Average was flat (-0.06%), while the Standard & Poor’s 500 edged higher by 0.82%. The Nasdaq Composite index gained 1.08% for the week. The MSCI EAFE index, which tracks developed overseas

stock markets, lost an eye-catching 5.72%.1,2,3

GEOPOLITICAL EVENTS

The build-up to Russia’s eventual invasion of Ukraine triggered elevated market volatility, resulting in broad-based selling that sent the S&P 500 into correction territory as the holiday-shortened week of trading

began.4

The sell-off culminated on Thursday morning following the overnight incursion of Russian troops into Ukrainian territory, though markets staged a powerful late-day recovery that coincided with President Biden’s

announcing fresh sanctions against Russia. The afternoon rebound was remarkable, as the S&P 500 ended 1.5% higher after being down more than 2.6%, while the Nasdaq Composite closed 3.3% higher after dropping nearly 3.5% intraday. Thursday afternoon’s momentum continued into Friday as stocks rallied to end the week in positive territory.5

INVASION IMPLICATIONS

Setting aside the more important aspects of the human cost and damage to world order, Russia’s invasion of Ukraine introduced an acute layer of uncertainty into many layers of the financial markets. The immediate

repercussion was the impact on global economic recovery due to rising energy prices, which reduce consumers’ discretionary spending and saddle businesses with higher costs.

The inflationary impact of higher energy and other prices, along with the prospect of decelerating economic growth, also complicates the Fed’s strategy to guide interest rates higher. Already, the probability of a 50

basis point interest rate hike at the Fed’s March 2022 meeting seems less likely than it was just a week ago. Finally, Russia’s actions have raised new concerns over second-order effects that could further unsettle markets, such as a new round of supply-chain disruptions.