would like to wish everyone Happy Holidays!

Happy Holidays from the Capstone Team!!

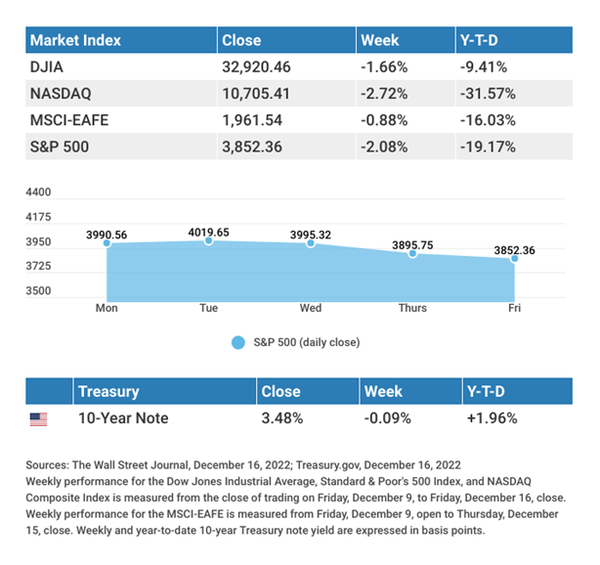

THE WEEK ON WALL STREET

Hawkish comments by the Fed and weak economic data heightened investors’ recession concerns and sent stocks lower last week.

The Dow

Jones Industrial Average lost 1.66%, while the Standard & Poor’s 500 retreated 2.08%. The Nasdaq Composite index declined 2.72% for the week. The MSCI EAFE index, which tracks developed overseas stock markets, slipped 0.88%.1,2,3

STOCKS UNDER PRESSURE

Stocks began the week on a positive note, supported by a

cooler-than-expected Consumer Price Index (CPI) report. Stocks reversed direction mid-week, however, following the Federal Open Market Committee (FOMC) meeting in which another 0.5% rate hike was announced.

The half-point increase was widely

anticipated, but the increase in the terminal rate (i.e., the point at which the Fed stops raising rates) rattled investors. Continued hawkishness by Fed Chair Powell at the post-meeting press conference added to investors’ anxiety. The potential for higher rates for longer, along with disappointing economic data, particularly a sharp decline in retail sales, amplified fears of a recession and sent stocks lower for the remainder of the week.

INFLATION AND THE FED

The release of November’s CPI showed inflation cooling for the second consecutive month, as prices rose just 0.1% month-over-month and 7.1% from a year ago. Both were better than expected.4

The FOMC ended its last meeting of 2022 by raising interest rates another 0.5% and signaling that it would likely continue to hike rates into the new year. At a subsequent press conference, Fed Chair Powell commented that the next rate increase could be a quarter-percentage point. Most FOMC members appear to support raising the terminal rate (the point at which hikes end)

to above 5%, up from its September projection of 4.6%.5