THE WEEK ON WALLSTREET

Stocks rallied last week, propelled by growing optimism overreaching a

deal on raising the debt ceiling and avoiding a technical debt default by the U.S.

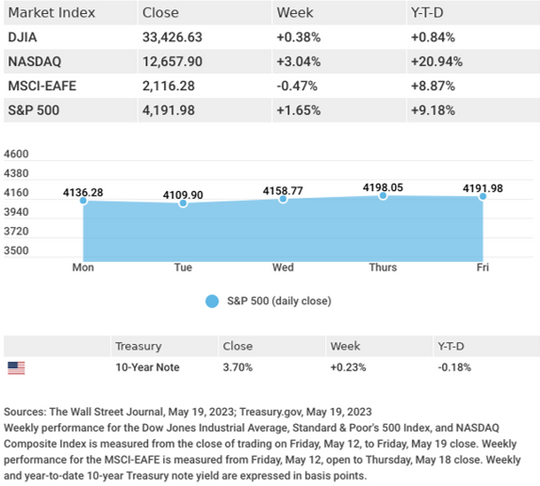

The Dow Jones Industrial Average edged 0.38% higher, while the Standard & Poor’s 500 gained 1.65%. The Nasdaq Composite index advanced 3.04% for the week. The MSCI EAFE index, which tracks developed overseas stock markets, lost 0.47%.1,2,3

POSSIBLE DEBT DEAL

After stumbling on weak April retail sales and a combination of disappointing earnings and weak guidance from a major retailer, stocks moved higher mid-week as the news on the debt negotiations turned more

positive.

The prospect of an agreement helped to lift a cloud of uncertainty that had weighed on markets in recent weeks and sparked sufficient optimism to shake off comments by the Dallas Fed President, who indicated that economic data may not support a pause in rate hikes yet. Aiding the market’s upbeat mood was a positive update on deposit growth at a troubled regional bank.

Stocks surrendered some of the week’s gains on Friday following reports of an impasse on debt talks and comments by Fed Chair Powell.

HOUSING MIXED

Recent updates have suggested that the housing market may be staging a turnaround after a long period of contraction. Last week’s data contained some fresh evidence of revival and caution that any potential recovery may remain further

out.

The first positive sign was an increase in home builder sentiment that put the National Association of Home Builders Housing Market Index’s confidence level at the midpoint for the first time since July 2022. An unexpected 2.2% rise in housing starts in April followed. These encouraging reports, however, were followed by a disappointing 3.4% decline in April existing home sales.4, 5, 6ays!